Biden Administration’s 2024 Regulatory Agenda

The below table contains a summary of some of the most significant agenda items for regulatory agencies that govern organizations in the financial services industry. Access to all the federal regulatory agenda items can be found here: Current Unified Agenda of Regulatory and Deregulatory Actions (reginfo.gov).

| Agency | Topic | Description | Stage |

|---|---|---|---|

| CFPB | Fair Credit Reporting Act | Rulemaking Key Objectives include change key defined terms, clarify permissible purpose, applicability of FCRA to data brokers and the sale of consumer data, prohibited marketing and advertising, processes to dispute accuracy, and to prohibit including consumer medical debt on consumer reports. | Considering developing a proposal |

| CFPB | Overdraft Fees | The Bureau is considering new rules regarding both overdrafts and insufficient funds (NSF) fees on its rulemaking agenda under regulation Z, and propose amendments how accounts can be overdrawn and how financial institutions determine whether to advance funds | Anticipate a proposal soon |

| CFPB | Section 1033: Personal Financial Data Rights | Process the comments received from the issued proposal, revised the proposal to incorporate changes it deems to be fit, and issue a final rule. | Anticipate a final rule in 2024 |

| CFPB | Supervision of Larger Participants in Consumer Payment Markets | The CFPB has defined larger participants in several markets and is considering issuing additional regulations to define further the scope of the CFPB’s nonbank supervision program. In particular, the CFPB is developing a proposed rule to define larger participants in a market for consumer payments. | Currently Developing a Proposal |

| CFPB | Amendments to FIRREA Concerning Automated Valuation Models | The agencies issued a proposed rule to implement the CFPA’s AVM amendments to FIRREA in June 2023. They would like to issue a final rule in 2024 | Anticipate a final rule in 2024 |

| CFPB | Registry of Nonbank Covered Persons Subject to Certain Agency and Court Orders | On January 30, 2023, the CFPB proposed a rule that would require certain nonbank covered persons that are under certain final public enforcement orders to register with the CPFB via a public registry, submit copies of public orders, prepare and submit written statements regarding such orders for use in connection with the CFPB’s supervisory functions. The public registry created by the CFPB would identify institutions subject to registration and include public enforcement orders and information regarding those orders. | Anticipate a final rule in 2024 |

| CFPB | Registry of Supervised Nonbank That Use Form Contracts to Impose Terms and Conditions That Seek to Waive or Limit Consumer Legal Protections | On February 1, 2023, the CFPB proposed a rule that would require certain supervised nonbank entities to register with the CFPB and provide information about their use of certain terms and conditions in standard-form contracts for consumer financial products or services that seek to waive or limit consumer rights or legal protections. The CFPB is looking to issue a final rule in 2024 | Anticipate a final rule in 2024 |

| CFPB | Credit Card Penalty Fees | On February 1, 2023, the CFPB proposed to (1) adjust the safe harbor dollar amount for late fees to $8 and eliminate a higher safe harbor dollar amount for late fees for subsequent violations of the same type; (2) provide that the current provision that provides for annual inflation adjustments for the safe harbor dollar amounts would not apply to the late fee safe harbor amount; and (3) provide that late fee amounts must not exceed 25 percent of the required minimum payment. | Anticipate a final rule in 2024 |

| FDIC, OCC, FED | Incentive-Based Compensation Arrangements | A joint proposed rule was issued to: (1) prohibiting incentive-based payment arrangements, (2) determine encourage inappropriate risks by certain financial institutions by providing excessive, compensation or that could lead to material financial loss; (3) requiring those financial institutions to disclose information concerning incentive-based compensation arrangements to the appropriate Federal regulator. | Anticipate a final rule in 2024 |

| FDIC, OCC, FED | Basel III Revisions: Amendments to the Capital Rule for Large Banking Organizations | Currently inviting public comments on a notice of proposed rulemaking (proposal) that would substantially revise the risk-based requirements applicable to the largest and most complex U.S. banking organizations as well as banking organizations with significant trading activity. | Anticipate a final rule in 2024 |

| FDIC, OCC, FED | Procedures for Monitoring Bank Secrecy Act Compliance | Speculation is centered around further development of proposals related to the beneficial ownership rule and other areas | Anticipate a final rule in 2024 |

| FDIC, OCC, FED | Long-term Debt Requirements for Large Bank Holding companies, and Large Insured Depository Institutions | Requesting comment on a notice of proposed rulemaking to consider whether the issuance of long-term debt by certain large banking organizations would enhance financial stability and enhance resolution options | Anticipate a final rule in 2024 |

| FDIC, OCC, FED | Resolution Plans Required for Insured Depository Institutions (Large Banks) | Seeking comment on a proposal to revise its rule currently requiring the submission of resolution plans by insured depository institutions (IDIs) with $50 billion or more in total assets. | Anticipate a final rule in 2024 |

| FDIC, OCC, FED | Proposed Amendments to the FDIC’s Section 19 Regulations | Section 19 requires persons with certain covered criminal offenses on their records to obtain prior written consent from the FDIC before participating in the conduct of the affairs of any insured depository institution. The agencies are requesting comments on proposed amendments to its section 19 regulations to create more flexibility to allow persons with records to potentially return to a FDIC insured institution. | Anticipate a final rule in 2024 |

| FDIC, OCC, FED | Guidelines Establishing Standards for Corporate Governance and Risk Management for Covered Institutions with Average Total Consolidated Assets of $10 Billion or More | The Proposed Guidelines would provide standards for corporate governance and risk management for covered institutions, including standards outlining the general obligations and duties of the board of directors, expectations for board composition and board committee structures and responsibilities, and expectations for the establishment of an independent risk management function incorporating a three lines-of-defense model. | Anticipate a final rule in 2024 |

| FDIC, OCC, FED | Quality Control Standards for Automated Valuation Models | Developing a rule to implement section 1473 of the Dodd-Frank Act concerning quality control standards for automated valuation models. | Anticipate a final rule in 2024 |

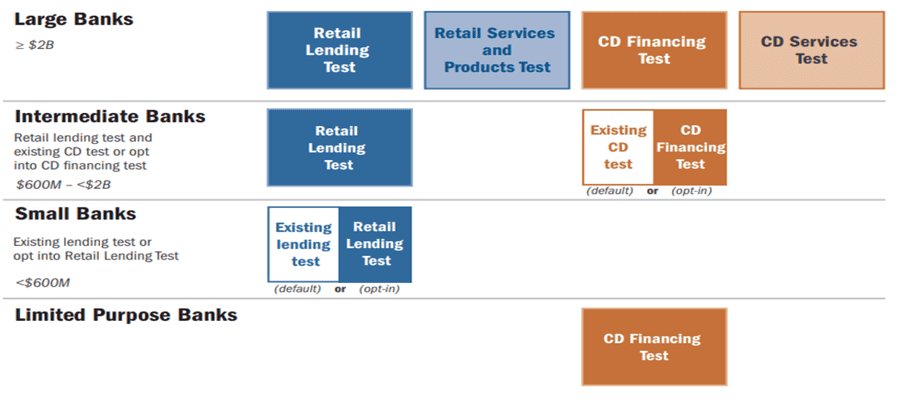

| FDIC, OCC, FED | Community Reinvestment Act | The final rule becomes effective in 2024, but most of the provisions won’t effective until 2026 and 2027. | Final Rule Effective, with many provisions deferred to 2026 and 2027 |

| FDIC, OCC, FED | Special Assessments Pursuant to Systemic Risk Determination | Will begin to impose special assessments on insured depository institutions to recover the loss to the Deposit Insurance Fund, starting January 1, 2024. No bank below the asset size of $5B will have to pay into the assessment. | Final rule effective 2024 |

| FED | Regulation Q–Regulatory Capital Rules: Risk-Based Capital Surcharges for Global Systemically Important Bank Holding Companies | Providing notice of the aggregate global indicator amounts for purposes of the calculation Global Systemically Important Bank surcharge rule | Anticipate a final rule in 2024 |

| NCUA | Simplification of Share Insurance Rules | The proposal would simplify the share insurance regulations by establishing a trust accounts category that governs coverage of shares of both revocable trusts and irrevocable trusts using a common calculation and provide consistent share insurance treatment for all mortgage servicing account balances held to satisfy principal and interest obligations to a lender. These amendments would be substantially similar to ones adopted by the Federal Deposit Insurance Corporation. | Anticipate a final rule in 2024 |

| NCUA | Overdraft Policy | The proposed rule would remove the 45-day limit and replace it with a requirement that the written policy must establish a specific time limit that is both reasonable and applicable to all members. | Anticipate a final rule in 2024 |

| NCUA | ACCESS Initiative: Chartering and Field of Membership (FOM) Regulations | The proposed regulatory amendments would remove outdated requirements, simplify the charter approval process, and clarify regulatory language. The Board will review the comments and consider final action. | Anticipate a final rule in 2024 |