The must anticipated Community Reinvestment Act (CRA) Interagency Final Rule was released on October 24, 2023. The release was the first time the rule had been revised in almost three decades. The final rule included a comprehensive overhaul of the requirements, including how banks will be evaluated. The Community Reinvestment Act (CRA) was created in 1977 and was designed to encourage banks to meet the credit needs of communities, with a strategic focus on low to moderate income communities. On April 1, 2024, the final rule and the public file requirements will be implemented. Banks have until January 1, 2026, to comply with most of the remaining provisions:

- New definitions

- Revised bank size and categories

- Designation of the eleven qualification criteria

- Interagency illustrative list of qualifying activities

- Retail lending assessment areas

- Receive credit for community development activities anywhere in the country, and

- data collection

The reporting requirements, for large banks only, will become effective on January 1, 2027, with the data to be reported no later than April 1, 2027. The final rule was designed to meet eight key objectives:

- CRA continues to be a strong and effective tool to address the credit needs of the underbanked and create innovative solutions to expand access to credit;

- Adapt to changes such as expanded role of mobile and online banking;

- Providing greater clarity, consistency, and transparency;

- Tailoring CRA evaluations and data collection to a bank’s size and business model;

- Tailor data collection and reporting requirements and use existing data whenever possible;

- Promote transparency;

- CRA and fair lending responsibilities are mutually reinforcing; and

- Promote a consistent regulatory approach.

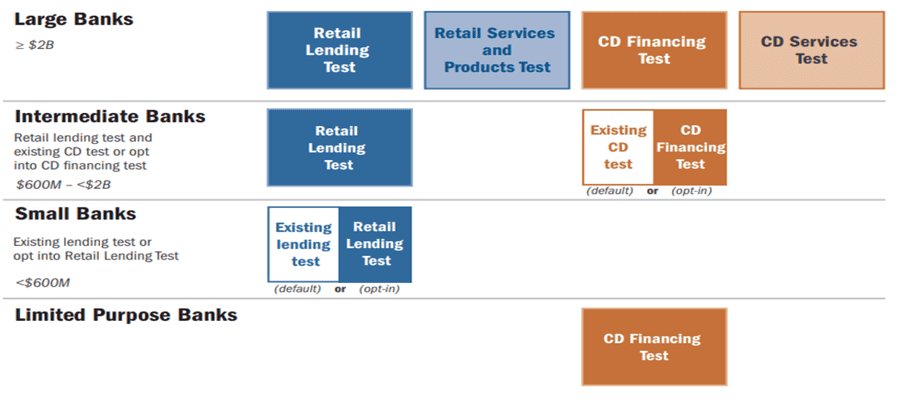

The size and category requirements in the final rule are listed in the figure below:

Each of the tests for large and intermediate banks are listed below:

- Large Banks: Retail Lending Test (40%), Retail Products and Services Test (40%), Community Development Financing Test (10%), and Community Development Servicing Test (10%).

- Intermediate Banks: Retail Lending Test (50%), and either the existing Community Development Test or the Community Development Financing test (50%).

Additional retail services and product evaluations will be required for banks over $10 billion. It would include an evaluation of their digital delivery systems, and the availability and usage of responsive deposit products. Other new requirements for large banks include creating a retail lending assessment area (RLAA). The RLAA is map of geographic areas where the bank has originated at least 150 closed-end mortgage loans or 400 small-business loans in each of the two prior calendar years. Banks are excluded from this requirement when they conduct 80% or more of specified retail lending activity inside of their facility-based assessment areas. Facility based assessment areas are still at the core of a CRA examination. The agencies will develop a publicly available illustrative list of qualifying CRA activities. Banks can request clarification from their regulator for activities not included on the illustrative list.

Leave A Comment